The S&P IPSA surged 1.89% to 11,217.82 on Wednesday, reclaiming the 11,200 level after Tuesday’s 2.14% rout — its worst session since the “Day of Liberation” selloff in April 2025. SQM-B led the rebound with gains of around 4%, followed by CMPC (~3.8%) and Mallplaza (~3%), as bargain hunters stepped in after the Latam Airlines secondary sale pressure dissipated. The recovery erased more than half of Tuesday’s losses but left the index still 4.3% below its January 28 all-time high of 11,721.38.

The Chilean peso strengthened 0.56% as the dollar fell to CLP 852.46 at close, powered by copper surging 3% to US$6.08 per pound. Supply disruptions and structural demand from the energy transition and AI data center buildout drove the metal to fresh highs, while the Dollar Index slipped 0.25% to 96.3. The peso has now appreciated 8.1% against the dollar over the past twelve months.

US nonfarm payrolls surprised to the upside at 130,000 — well above the 70,000 consensus — but annual benchmark revisions slashed 898,000 jobs from the 2025 count. The delayed report (pushed back by a partial government shutdown) showed unemployment ticking down to 4.3% and wages rising 0.4% monthly. Health care and social assistance accounted for 95% of January’s gains, while federal government payrolls fell 34,000 as deferred resignations from 2025 took effect.

| Indicator | Close | Change |

|---|---|---|

| S&P IPSA | 11,217.82 | +1.89% |

| USD/CLP (Dow Jones avg) | 852.46 | −0.56% |

| USD/CLP (Pepperstone close) | 853.72 | −0.33% |

| Copper (LME 3-mo) | ~US$6.08/lb | +3.0% |

| DXY (Dollar Index) | 96.30 | −0.25% |

Chilean equities staged a forceful recovery on Wednesday as the S&P IPSA climbed 1.89% to close at 11,217.82, reclaiming the psychologically important 11,200 level after Tuesday’s 2.14% plunge — the index’s steepest single-day decline since Trump’s “Day of Liberation” tariff shock on April 7, 2025. The session opened at 11,009.28 (Tuesday’s close) and pushed steadily higher throughout the day, reaching an intraday high of 11,221.11 before settling just below.

The rebound was broad-based but led by the same names that had dragged the index lower in recent sessions. SQM-B rose approximately 4%, recovering part of its losses from the ongoing Tianqi Lithium overhang — the Chinese shareholder (21.9% stake) announced on February 4 that it intends to sell up to 3.57 million Class A shares (1.25% of SQM’s total). CMPC gained 3.8% and Mallplaza added 3%, while Cencosud rose 2.3% and Itaú Chile climbed 2.8%. Among the laggards, Latam Airlines traded near CLP 26.55, still digesting the US$742.8 million secondary sale by Sixth Street Partners — the fund’s sixth liquidation under the Registration Rights Agreement dating from Latam’s Chapter 11 reorganization.

The Latam sale — 12 million ADR at US$61.90 each, underwritten by J.P. Morgan — settled on Wednesday. With the transaction, Sixth Street’s stake fell from 17.4% to 13.2%. Analysts at Bci Corredor de Bolsa maintained their CLP 34 price target, noting the discount represented an attractive entry point, while Credicorp Capital’s Ignacia Montt linked the recent price correction to anticipation of the secondary sale.

Meanwhile, the Telefónica Chile saga reached its conclusion. On Tuesday, Telefónica Spain confirmed the sale of 100% of its Chilean operations to a consortium of NJJ Holding (51%) and Millicom/Tigo (49%) for US$1,215 million, plus a conditional earn-out of up to US$150 million. The deal, which closed simultaneously with signing, ends 35 years of Telefónica’s presence in Chile. The new CEO — Carolina Vallejo Londoño, formerly Millicom’s Tigo CEO in El Salvador — was appointed immediately. Entel, the incumbent most exposed to competitive disruption from a reinvigorated Movistar/Tigo, saw its shares fall 12.6% on Tuesday (its worst session since March 2020) and remained under pressure on Wednesday at −1.6%.

The peso extended its appreciation trend on Wednesday, with the dollar closing at CLP 852.46 on the Dow Jones average — down 0.56% from Tuesday’s 857.23. On the Pepperstone feed, USD/CLP settled at 853.72 after opening at 852.80 and trading in a tight 851.51–858.59 range. The dollar has fallen 1.73% against the peso over the past week and 8.12% over the past twelve months.

The primary tailwind was copper. The metal surged 3% to approximately US$6.08 per pound on the LME, maintaining its position above US$13,000 per metric ton. Felipe Sepúlveda of Admirals Latinoamérica attributed the rally to “supply disruptions combined with robust structural demand from the energy transition and the expansion of AI-linked data centers.” Cochilco’s latest daily report (February 10) showed LME spot copper at 589.76 ¢US$/lb (US$13,002/t) and three-month futures at 594.12 ¢US$/lb (US$13,098/t), with the year-to-date average at 592.97 ¢US$/lb.

The Dollar Index contributed to peso strength, falling 0.25% to 96.3 after the mixed US jobs data: while the headline 130,000 payroll figure beat expectations, the massive 898,000 downward revision to 2025 employment reinforced the narrative of a decelerating labor market. Markets now price nearly 40% odds of three Fed rate cuts this year, up from the prior expectation of two. Cochilco projects copper averaging US$4.95/lb for 2026, though spot prices have consistently traded above that forecast.

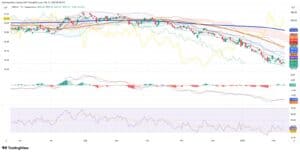

Wednesday’s 1.89% bounce produced a solid green candle that recovered the 11,200 zone, though the index remains in the correction channel that began after the January 28 all-time high of 11,261.90. The session opened at 11,009.28 (Tuesday’s close — also the intraday low) and rallied to a high of 11,221.11 before closing at 11,217.82, just below the recent swing high near 11,261.

The moving average structure remains constructive. Price is trading well above the 200-day SMA at 9,218.89 (nearly 22% below current levels), confirming the primary uptrend is intact. The EMA cluster near 10,824–10,968 provides the first meaningful dynamic support band, while the Ichimoku cloud’s upper boundary near 10,835 acts as a further structural floor.

Momentum indicators are mixed. The RSI stands at 65.75/51.96 — the primary reading in the upper neutral zone while the smoothed line sits at mid-range, suggesting the index is neither overbought nor oversold after the recent correction. The MACD histogram at −83.20 remains in negative territory with the signal lines at 194.08/110.87, indicating that while the longer-term trend is bullish (both lines well above zero), near-term momentum has weakened since the January highs.

| Level | Value | Significance |

|---|---|---|

| All-Time High | 11,721.38 | Jan 28 intraday peak |

| Recent Swing High | 11,261.90 | Immediate resistance |

| Close | 11,217.82 | Feb 11 close |

| Psychological | 11,000 | Round-number support |

| EMA Cluster | 10,824–10,968 | Dynamic support zone |

| 200-Day SMA | 9,218.89 | Structural trend support |

The peso’s appreciation trend accelerated on Wednesday, with the pair closing at 853.72 after trading in a 851.51–858.59 range. The candle formed a modest bullish reversal for the dollar intraday (the close was above the low), but the broader trend remains decisively bearish for USD/CLP — the pair is trading far below all major moving averages.

The 200-day SMA at 935.46 sits nearly 10% above spot, underscoring the magnitude of the peso rally since mid-2025. The EMA cluster in the 887–897 range provides the first major overhead resistance zone, with the Bollinger Band midline near 877 acting as an intermediate ceiling. The Ichimoku cloud, now visible above price in the 860–870 zone, confirms the bearish regime for the dollar.

The RSI at 36.28/33.97 is approaching oversold territory, with the smoothed reading at its lowest levels since the current peso bull run began. However, in strong trends, oversold readings can persist for extended periods. The MACD histogram is barely positive at 0.30 with signal lines at −11.09/−11.39 — deeply negative but showing the first hints of a potential momentum base, suggesting the downside pace may be moderating even as the structural trend remains peso-positive.

| Level | Value | Significance |

|---|---|---|

| 200-Day SMA | 935.46 | Major structural resistance |

| EMA Cluster | 887–897 | Overhead resistance zone |

| Bollinger Midline | ~877 | Dynamic mean reversion |

| Ichimoku Cloud | 860–870 | Nearest overhead barrier |

| Close | 853.72 | Feb 11 close |

| Cycle Low | 846.26 | Lower Bollinger Band |

The US employment report dominated the macro calendar. The Bureau of Labor Statistics reported 130,000 nonfarm payrolls for January 2026, well above the 70,000 consensus and the strongest month since December 2024. Health care led with 82,000 jobs, followed by social assistance (42,000) and construction (33,000). Average hourly earnings rose 0.4% monthly and 3.7% year-over-year, both above estimates. The unemployment rate ticked down to 4.3% from 4.4%.

But the real story was the benchmark revisions. Total 2025 employment growth was slashed from 584,000 to just 181,000, an 898,000 downward adjustment — the second-largest negative revision on record after the 2009 financial crisis. Average monthly payroll gains for 2025 fell from 49,000 to just 15,000. As Barry Ritholtz of The Big Picture noted, hiring breadth was “alarmingly narrow,” with health care and social assistance accounting for 95% of January’s gains. Federal government employment fell 34,000 and is now down 327,000 (−10.9%) from its October 2024 peak.

For Chile, the implications are asymmetrically positive. A weaker US labor market supports the case for continued Fed easing — markets now price nearly 40% odds of three rate cuts in 2026, up from two previously — which tends to weaken the dollar and channel flows into emerging market assets and commodities. The Banco Central de Chile’s monetary policy rate remains at 4.5% (held steady on January 27 after a cut in December 2025), and with annual inflation at just 2.8% as of January — below the 3% target for the first time in nearly five years — the positive carry and copper tailwind are structural supports for the peso.

Wednesday’s session delivered the kind of V-shaped recovery that confirms the IPSA’s structural bull market remains intact. The 1.89% bounce — reclaiming more than half of Tuesday’s 2.14% loss in a single session — speaks to the depth of buying interest that materializes on dips toward 11,000. The market has now successfully defended this level twice in February, establishing it as the floor for the current consolidation range.

The twin catalysts of the Latam secondary sale (now settled) and the Telefónica Chile acquisition (now closed) have been absorbed with remarkable speed. The Latam overhang specifically should diminish: Sixth Street is down from its post-reorganization peak to 13.2%, and each successive sale narrows the remaining supply. For Entel, however, the Millicom/NJJ entry represents a genuine competitive threat — a well-capitalized new owner with Latin American scale replacing a departing Telefónica that had been in maintenance mode.

Technically, the IPSA’s RSI at 65.75 has room to run before hitting overbought territory, while the MACD histogram at −83 suggests the correction’s momentum is fading. The base case is a test of the 11,261 swing high in the near term, with the all-time high of 11,721 as the medium-term target if copper sustains above US$6/lb and the global risk appetite holds. For USD/CLP, the oversold RSI at 34 argues for a tactical dollar bounce toward 860–870, but the structural trend remains firmly peso-positive as long as copper stays elevated and the Fed remains on a dovish trajectory. The range to watch: IPSA 11,000–11,260 and USD/CLP 846–870.

Report compiled by The Rio Times • Data sources: Bolsa de Santiago, LarrainVial, Infobae, Diario Financiero, Diario Estrategia, TradingView, Cochilco, BLS, CNBC • Charts: TradingView (Pepperstone) • Published February 12, 2026