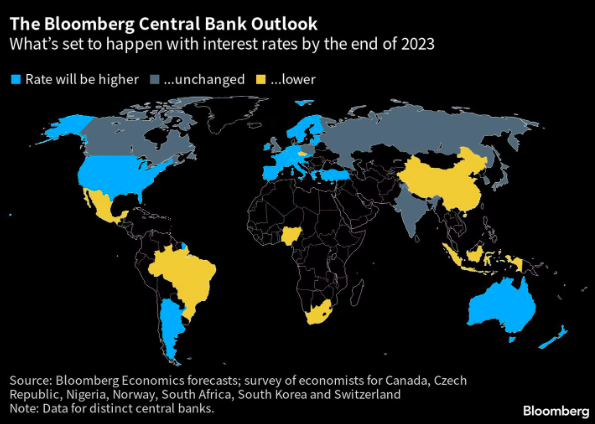

Most of the world’s central banks may be close to peaking or have already finished raising their interest rates, portending a hiatus before possible monetary easing appears on the horizon.

With early signs of weakening economic growth already visible and the aftermath of financial market stress still lingering, any pause by the Fed after at least one more hike in May could cement a turnaround after the most aggressive monetary policy the world has seen in decades.

The European Central Bank and its regional counterparts could go longer and even aim to maintain restrictive levels.

Still, a US monetary policy reversal led by Chairman Jerome Powell would be an important signal to their global counterparts.

From Brazil to Indonesia, the shift toward rate cuts could begin as early as this year, and many developed country officials would not be far behind.

Overall, at least 20 of the 23 major jurisdictions tracked by Bloomberg are expected to reduce borrowing costs by 2024.

According to an indicator calculated by Bloomberg Economics, global rates will peak at 6% in the third quarter.

By the end of next year, that measure is expected to fall to 4.9%.

As in previous cycles, Japan will likely stand out from the rest.

Under newly installed Governor Kazuo Ueda, its interest rate – currently the lowest in the world – is expected to remain unchanged until next year, when it is finally scheduled to rise to zero.

What Bloomberg Economics says:

“Since the beginning of the year, central banks have been buffeted by contradictory forces. China’s rapid reopening, Europe’s dodging a recession, and tightening US labor markets argue for a rate hike.”

“The collapses of Silicon Valley Bank and the sale of Credit Suisse pull in the opposite direction.”

“So far, with little sign of a broader banking crisis, the tightening case is winning the day.”

“Peak rates are in sight, but we’re not there yet,” according to Tom Orlik, the chief economist.

Here is Bloomberg’s quarterly guide to some of the world’s major central banks.

GROUP OF SEVEN

US Federal Reserve

- Current federal funds rate (upper bound): 5%.

- Bloomberg Economics forecast for the end of 2023: 5.25%.

- Bloomberg Economics forecast for end-2024: 4.25%.

Despite recent banking strains, Fed policymakers are on track to continue raising rates, with rising oil prices likely to reinforce their decision to hike rates at their early May meeting.

While policymakers stress the need for patience in assessing what the collapse of the SVB means for the US economy, there has been little change in their rhetoric about the need to cool price pressures.

That said, financial conditions have tightened in the wake of SVB’s collapse, and officials are not ruling out that this will help slow the US economy, which could reduce the need for further hikes.

Investors expect rates to peak below 5%, with the Fed cutting them by about 50 basis points before the end of 2023.

European Central Bank (ECB)

- Current deposit rate: 3%.

- Bloomberg Economics forecast for the end of 2023: 3.5%.

- Bloomberg Economics forecast for end-2024: 2.5%.

ECB policymakers are increasingly warning that their most aggressive period of hikes may be coming to an end.

Some lower ones are likely to be maintained to cope with core inflation, which broke another record in March and will remain elevated.

However, with headline price increases back on track toward the 2% target, most of the tightening – 350 basis points since last July – has been completed.

Bank of Japan (BoJ)

- Official interest rate: -0.1%.

- Bloomberg Economics forecast for end-2023: -0.1%.

- Bloomberg Economics forecast for the end of 2024: 0%.

The Bank of Japan is now led by its first new Governor in a decade.

This quarter will be key in setting the tone for Kazuo Ueda’s five-year term.

So far, he has given strong signals of maintaining stimulus. Still, market attention is focused on whether and when the veteran economics professor will adjust the BOJ’s yield curve control.

June is the most popular time for a policy change among BOJ watchers, but there is little doubt that Ueda will be under intense scrutiny at his first meeting later this month.

Bank of England (BoE)

- Current Bank Rate: 4.25%.

- Bloomberg Economics forecast for end-2023: 4.25%.

- Bloomberg Economics forecast for end-2024: 3.5%.

An unexpected pickup in UK inflation has divided economists and investors over whether the Bank of England will continue its fastest monetary tightening in three decades.

Money markets anticipate that a final quarter-point rate hike to 4.5% by mid-year is more likely, but economists are marginally leaning against any further change.

SOME OF THE BRICS

People’s Bank of China

- Current 1-year medium-term lending rate: 2.75%.

- Bloomberg Economics forecast for end-2023: 2.55%.

- Bloomberg Economics forecast for end-2024: 2.45%.

China’s economic recovery is gaining momentum following the abrupt removal of Covid restrictions and stabilizing the property market. However, the rebound remains uneven, and policymakers do not intend to reduce monetary support.

Instead of interest rates, the PBOC is using other policy tools, such as the reserve requirement ratio-which it cut in March, to help stimulate economic credit and growth.

Central Bank of Brazil

- Current Selic target rate: 13.75%.

- Bloomberg Economics forecast for end-2023: 12%.

- Bloomberg Economics forecast for end-2024: 9%.

Brazil’s central bank has not indicated that it is ready to lower its benchmark interest rate from a six-year high, defying intense political pressure for looser monetary policy.

While President Luiz Inacio Lula da Silva, his economic team, and many business leaders complain that borrowing costs are choking Latin America’s largest economy, the central bank insists that the cost of bringing inflation down to target would be even higher in the future if they faltered now in their fight.

The autonomous monetary authority led by Roberto Campos Neto has held the benchmark Selic steady at 13.75% for five consecutive meetings after raising it from a record low of 2% during the pandemic.

Even with inflation slowing for ten straight months in mid-March, the central bank is still trying to cool the services sector while fighting a recent rise in inflation expectations for the next three years.

OTHER CENTRAL BANKS IN LATAM

Bank of Mexico

- Current overnight interest rate: 11.25%.

- Bloomberg Economics forecast for end-2023: 10.75%.

- Bloomberg Economics forecast for end-2024: 6.75%.

The Bank of Mexico is nearing the end of its tightening campaign after raising the benchmark rate for 15 consecutive meetings to 11.25%.

Banxico, as the central bank is known, slowed the rate hikes on March 30 with a quarter-point increase that could be the last.

Inflation figures released after that decision provided relief: consumer prices rose in March somewhat less than economists had expected, although underlying measures slowed less than expected.

Central Bank of Argentina

- Current minimum rate: 78%.

- Bloomberg Economics forecast for end-2023: 80%.

- Bloomberg Economics forecast for end-2024: 70%.

Argentina’s central bank resumed tightening monetary policy in March, a month after annual inflation surpassed 100%.

As prices continue to rise ever faster, the International Monetary Fund is urging policymakers to raise rates further ahead of October’s presidential election.

With information from Bloomberg